How the Iran War and Oil Price Shock Are Affecting Vancouver Real Estate in 2026

Oil prices have surged over 55% since the Iran conflict escalated. Here's how that geopolitical shock is filtering into Vancouver's mortgage rates, buyer demand, and home prices right now.

When conflict breaks out halfway around the world, it can be easy to assume that the local real estate market is insulated from the fallout. But in Vancouver, one of the most globally connected housing markets in Canada, what happens in the Strait of Hormuz does not stay in the Strait of Hormuz.

The war involving Iran that escalated sharply in early 2026 has sent oil prices surging, rattled bond markets, and forced a reassessment of Canada's interest rate trajectory. For anyone thinking about buying, selling, or renewing a mortgage in the Lower Mainland this spring, understanding this chain of events is not just useful background knowledge. It is essential context for making sound decisions.

This post breaks down exactly what is happening, how the effects are flowing through to Vancouver, and what it means for you.

What Has Happened With Oil Prices

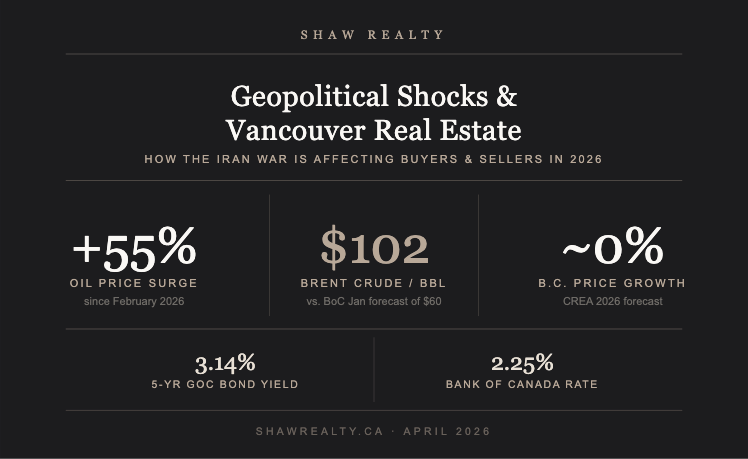

The numbers are striking. Brent crude oil was trading around $72 per barrel in late February 2026. By early April it had hit nearly $120 per barrel, a surge of more than 55% in roughly six weeks. That ranks among the largest monthly oil price jumps on record.

The driver is the Strait of Hormuz, the narrow waterway through which approximately 20% of the world's seaborne oil trade passes. Disruptions and outright closures of this critical chokepoint have choked global oil supply, triggered panic buying in energy markets, and put sustained upward pressure on fuel and energy costs worldwide.

Gasoline prices in Canada have already reflected this shock. The national average climbed to roughly $1.80 per litre by early April, near annual highs. In Metro Vancouver, where fuel costs were already among the highest in North America before the conflict, the hit to household budgets has been immediate and tangible.

As of mid-April, there are early signals that U.S. and Iranian officials may be discussing an end to the conflict, and Brent briefly dipped below $100 per barrel on that news. But markets remain volatile, and the energy disruption is already baked into the economic data.

The Transmission Mechanism: How Oil Prices Reach Your Mortgage

This is the part most buyers and sellers do not fully appreciate. Rising oil prices affect Vancouver real estate not through some vague sense of economic unease, but through a very specific and well-understood chain of events.

Step 1: Inflation Rises

Higher fuel costs are not just felt at the gas pump. The cost of trucking groceries, manufacturing building materials, shipping goods, and running virtually every business with a physical footprint all increase in tandem with oil prices. This shows up quickly in headline inflation figures. Canada's March 2026 inflation reading came in at 2.4%, and analysts expect it to climb further if oil prices remain elevated.

Step 2: Bond Markets Reprice

Bond investors hate inflation. When inflation expectations rise, they demand higher yields on government bonds to compensate for the erosion of their returns. This has already played out in real time: the Government of Canada 10-year bond yield climbed to approximately 3.50% in March, a meaningful increase from where it started the year. The 5-year GoC benchmark bond yield, which is the primary driver of fixed mortgage rates in Canada, is hovering near 3.14%.

Step 3: Fixed Mortgage Rates Rise

Fixed mortgage rates in Canada are priced off GoC bond yields, not directly off the Bank of Canada's overnight rate. When bond yields jump, fixed mortgage rates follow within days or weeks, regardless of what the central bank does. This is precisely what happened in March: fixed mortgage rates rose sharply as a direct result of the bond yield surge tied to the Iran conflict escalation.

Step 4: Buyer Purchasing Power Contracts

Higher fixed mortgage rates mean higher monthly carrying costs for the same purchase price. A buyer who qualified for a $900,000 purchase at a 4.5% five-year fixed rate may find themselves several thousand dollars per month worse off at 5.2%. That difference compresses the pool of qualified buyers and, over time, puts downward pressure on prices.

What This Means for the Bank of Canada

The Bank of Canada finds itself in an uncomfortable position. It had spent much of 2025 cutting rates to support a slowing economy, bringing the overnight rate down to 2.25% by early 2026. The logic was sound: Canada's economy was absorbing the shock of U.S. tariffs, population growth was slowing, job losses were mounting, and GDP contracted at a 0.6% annualized rate in Q4 2025.

Then the oil shock arrived.

The Bank now has to weigh persistent inflationary pressure from energy prices against a genuinely weak domestic economy. Most major bank economists, including those at CIBC, RBC, TD, and National Bank, are forecasting the overnight rate will hold at 2.25% through 2026, though that consensus has become less certain in recent weeks. Scotiabank is an outlier, forecasting a potential hike to 3.00% by year-end if inflation proves stubborn.

The Bank's January forecast assumed Brent crude at $60 per barrel. With the benchmark recently trading above $100, that forecast is significantly outdated. Governor Macklem has signalled awareness of rising inflation risks, but has stopped short of committing to rate hikes given how weak the broader economic backdrop is.

The practical implication for borrowers is this: the rate relief that many Canadians were counting on in 2026 may not materialize in the form expected. And if the Bank does pivot to hikes, or if bond yields remain elevated, fixed mortgage rates could stay high or move higher for the balance of the year.

The Vancouver Picture Specifically

Vancouver's housing market was already navigating a complex set of conditions before the geopolitical shock arrived. The CREA MLS Home Price Index had fallen for 16 consecutive months through March 2026. The national average home price was $673,084 in March, down 0.8% year over year. CREA's forecast for B.C. specifically calls for virtually no price growth in 2026 on an annual basis.

That forecast was issued before the full oil shock was absorbed. CREA senior economist Shaun Cathcart told CBC News that the association has had to lower its housing activity forecast because of the situation in the Middle East and the oil shock.

In the condo market, conditions are particularly soft. Vancouver's apartment segment, which had been under sustained pressure from investor exit and a surge in new completions, is not well-positioned to absorb additional headwinds to buyer purchasing power and consumer confidence.

The detached and townhouse segments in the suburbs, which were showing early signs of stabilization, are now facing renewed uncertainty as buyers reassess affordability in a higher-rate environment.

There are also secondary effects worth noting for Vancouver specifically:

Construction costs: Rising fuel and materials costs affect the cost of new construction. If oil prices remain elevated, the cost of framing lumber, drywall, and concrete all rise. This is a long-term factor supporting prices on the supply side, but it does nothing to help affordability in the short term.

Consumer confidence: Vancouver buyers are highly sensitive to economic uncertainty. The combination of a global conflict, market volatility, and rising household costs at the pump and grocery store tends to push buyers and sellers to the sidelines. Fewer transactions mean thinner markets and less reliable pricing signals.

The immigration and population tailwind: Metro Vancouver has long benefited from strong population growth as a sustained source of housing demand. That tailwind has moderated, but it has not disappeared. Any eventual stabilization in oil prices and bond markets will likely see pent-up demand release relatively quickly into this market.

A Note on the Historical Pattern

It is worth stepping back for perspective. Major geopolitical shocks have, historically, created significant short-term volatility in Canadian housing markets without derailing the long-term trajectory. The energy crisis of the early 1970s, the Gulf War of 1990, and the post-9/11 uncertainty all created periods of hesitation followed by recovery.

What distinguishes the current moment is the simultaneous presence of multiple pressures: U.S. tariff uncertainty affecting Canadian exports, a domestic economy that was already contracting before the oil shock, an elevated cost of living that has eroded household savings buffers, and now an energy price surge that is pushing inflation back up at exactly the wrong moment.

None of this means the market is headed for a dramatic crash. But it does mean that the easy optimism of late 2025, when many were predicting a robust spring recovery in 2026, needs to be recalibrated.

What Should Buyers Do Right Now?

Get pre-approved and lock in a rate. Fixed mortgage rates are volatile. A rate hold from a lender typically gives you 90 to 120 days of protection. If you are planning to buy this spring or summer, getting pre-approved now locks in today's rate even if rates rise further before you find a property.

Understand your full carrying cost. In a world where gasoline is $1.80 per litre and grocery prices are rising, your mortgage payment is only one component of ownership cost. Run your numbers with a realistic cost-of-living buffer, not 2023 assumptions.

Think long-term on the buy decision. If you are buying a home you intend to live in for seven or more years, short-term market volatility matters less than the long-term fundamentals of Vancouver: geographic constraints on supply, continued (if moderated) immigration, and a globally desirable quality of life. The market will recover. The question is timing relative to your personal situation.

Consider condos carefully. The condo correction in Vancouver is real and ongoing. Buyers entering the apartment segment should be aware they may be buying into a market that has not yet fully repriced. That creates opportunity for those with long time horizons, but it requires eyes-open analysis.

What Should Sellers Do Right Now?

Price to the current market, not the 2022 market. Overpriced listings in this environment sit, accumulate days on market, and ultimately sell for less than they would have at a correctly calibrated initial price. Buyers in a volatile market are cautious. Give them a reason to act.

Presentation matters more in a buyer's market. When inventory is higher and buyers have more choice, the condition, staging, and photography of your listing do material work in attracting qualified interest. This is not the market to cut corners on preparation.

Consider your timing in the context of your next move. If you are selling and buying, understand that both transactions are happening in the same market. The discount you may take on your sale may also be available on your purchase.

The Bottom Line

The Iran conflict and the resulting oil price shock are not abstract geopolitical events. They have already translated into higher bond yields, rising fixed mortgage rates, dampened buyer confidence, and a downward revision to housing market forecasts across Canada, including in B.C.

Vancouver's market was already navigating a period of adjustment before this shock arrived. The spring of 2026 is shaping up to be slower and more uncertain than many hoped. That does not mean opportunities are absent. It means they require more careful analysis and a clear understanding of the forces at play.

If you are trying to make sense of what this means for your specific situation, whether you are thinking about buying your first home, downsizing, selling an investment property, or navigating a renewal, I am happy to have a conversation.

Ian Shaw is a Vancouver real estate agent specializing in the Greater Vancouver and Lower Mainland market, with a particular focus on helping homeowners navigate major life transitions including downsizing. You can reach him at ian@shawrealty.ca or through shawrealty.ca.

Sources:

- CNBC, "A timeline of how the Iran war shook oil prices," April 21, 2026

- CBC News, "CREA downgrades housing market forecast due to oil shock," April 2026

- Canadian Mortgage Trends, "Bank of Canada likely to stay on hold as oil scrambles the outlook," March 18, 2026

- Largo Capital, "Canada's Real Estate Market in March 2026," March 2026

- True North Mortgage, Mortgage Rate Forecast, April 2026

- Rates.ca, Mortgage Rate Forecast, April 2026

- RBC Economics, "Why the oil price shock isn't likely to reignite broad inflation in Canada," April 2026

Categories

Recent Posts